1.1 Asset Management Framework

1.2 Utilizing Benefits of Asset Management

1.1 Asset Management Framework

1.2 Utilizing Benefits of Asset Management

The Asset Management Framework has been prepared to assist Ontario municipalities assess and improve their maturity level in all aspects of asset management planning. While most Ontario municipalities already have an Asset Management (AM) plan, many may be unsure on how to best use it or if it meets the needs of the municipality. This document provides guidance to municipalities on how to move through the AM continuum, and how to progress towards meeting the municipality’s objectives through effective and efficient management of all its assets.

Structure of Framework

This Framework is organized as follows:

Chapter 1: Introduction;

Chapter 2: Asset Management Policies and Strategies;

Chapter 3: State of Local Infrastructure;

Chapter 4: Levels of Service Analysis;

Chapter 5: Lifecycle Management Strategy;

Chapter 6: Financing Strategy;

Chapter 7: Asset Management Integration;

Chapter 8: Continuous Updates and Improvements;

Chapter 9: Asset Management Tools;

Chapter 10: Internal Governance and Ownership;

Chapter 11: Council Approval and Support; and

Chapter 12: Public Engagement and Consultation.

Overview of Chapters:

Chapter 2: Asset Management Policies and Strategies

Explains how asset management should be viewed as a process, supported by

policies and strategies for meeting AM objectives effectively.

Chapter 3: State of Local Infrastructure

Provides a discussion on capital asset information collection, storage, and use.

The discussion relates to a municipality’s asset inventory, including asset

attributes, accounting valuations, current valuations, condition assessments,

service potential, risk assessments, and data integrity. This information

provides the foundation for other sections of an AM plan.

Chapter 4: Levels of Service Analysis

Examines the identification of services, community expectations, strategic (or community)

based levels of service, technical levels of service, and the comparison of

current service levels to expected levels of service. In addition, budget

impacts of the levels of service analysis and the importance of measuring

trends and performance are explained.

Chapter 5: Lifecycle Management Strategy

Provides a foundation for developing a municipality’s long-term operating and

capital forecast for asset related costs. This includes the requirements for

non-infrastructure solutions, maintenance and operation, rehabilitation, replacement/disposal,

and expansion of the municipality’s asset base while moving towards the

expected levels of service. The goal of a lifecycle management strategy is to

have the municipality in (or moving towards) a sustainable asset management

position.

Chapter 6: Financing Strategy

Identifies concepts and strategies for long-term funding plans for the

lifecycle management strategies. This includes consideration of rate impacts,

available funding sources, infrastructure funding deficits/shortfalls,

performance and sustainability measures, and reporting options.

Chapter 7: Asset Management Integration

Describes how AM can be integrated into the budget process, strategic planning,

PSAB 3150 compliance, and other relevant organizational processes.

Chapter 8: Continuous Updates and Improvements

Discusses processes and tools available for incorporating improvements and

updates to the AM process.

Chapter 9: Asset Management Tools

Provides guidance related to the selection and utilization of beneficial AM

software and related tools.

Chapter 10: Internal Governance and Ownership

Outlines the importance of supporting AM through the municipality’s

organizational structure, leadership through senior management, and allocating sufficient

AM resourcing levels.

Chapter 11: Council Approval and Support

Discusses the significance of achieving and maintaining council approval and

support throughout the AM process.

Chapter 12: Public Engagement and Consultation

Highlights the advantages of involving the public in the AM process.

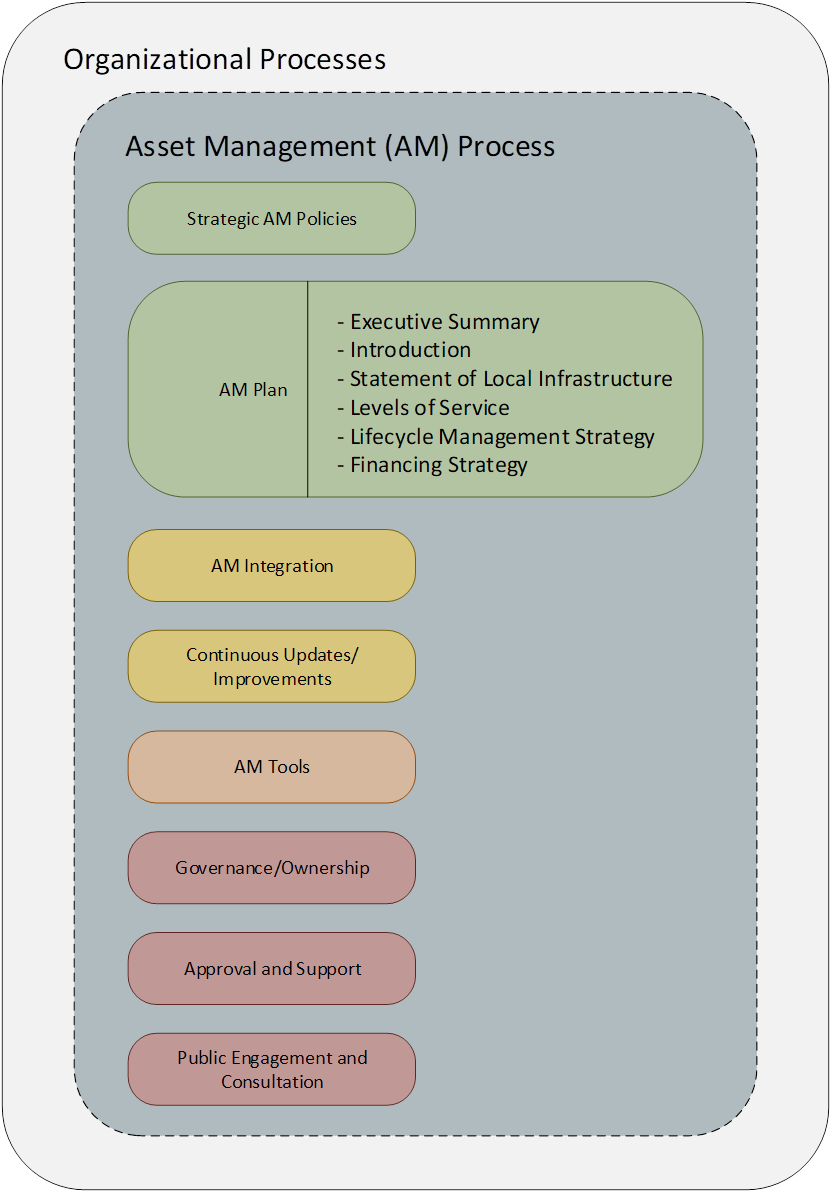

Figure 1-1 (below) shows the flow of these chapters in the context of the framework:

Figure 1‑1

Asset Management Framework

It is important to note that Figure 1-1 (above), and the chapters within this document, consist of much more than the steps to create an AM plan. Chapters 3 through 6 (State of Local Infrastructure, Levels of Service Analysis, Lifecycle Management Strategy, and Financing Strategy) form the basis for an AM plan. This document treats asset management as a process, with one portion of that process being the creation of an AM plan.

In addition, an effective asset management process involves processes, people, and technology to provide expected levels of services to the community. It is the culmination of all of these variables that makes asset management effective.

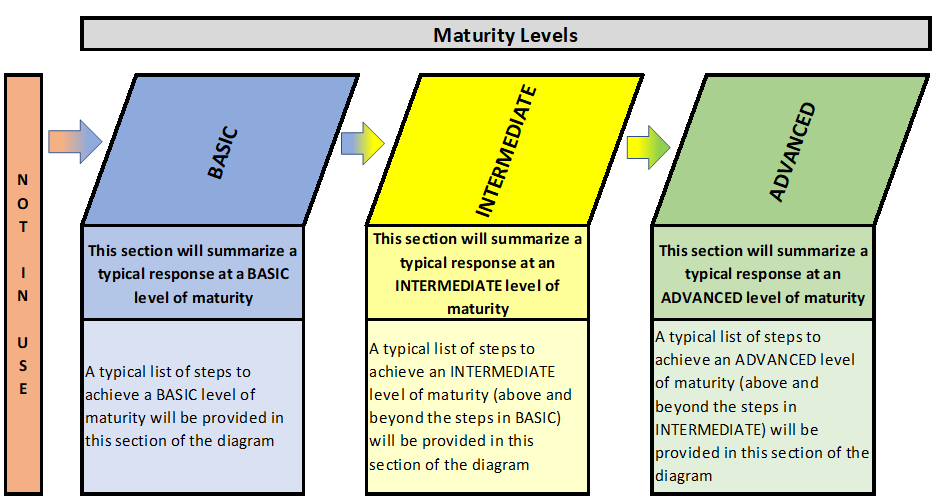

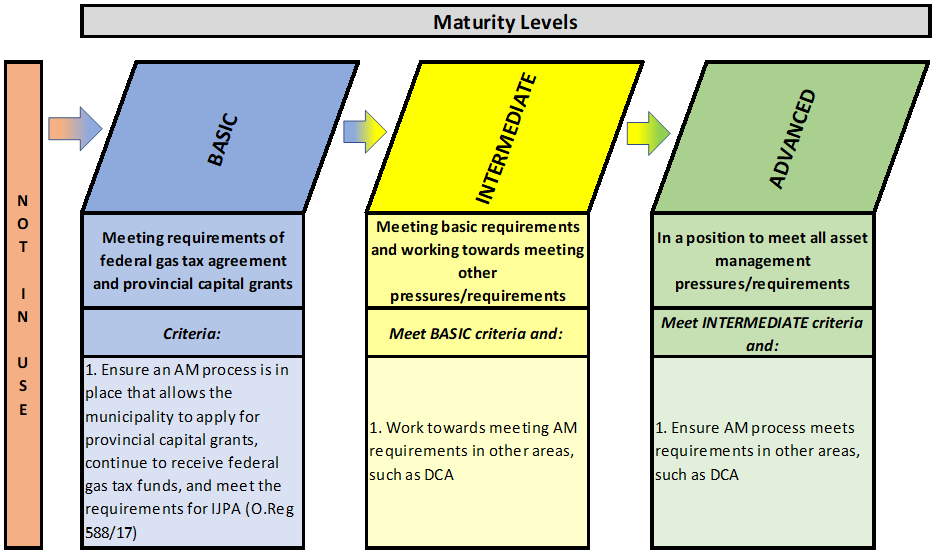

Level of Maturity Diagrams

This framework is intended for municipalities of all sizes and maturity levels. The use of the maturity diagrams within this framework can help municipalities identify their current levels of maturity for each AM area. In addition, the diagrams provide possible approaches for municipalities to undertake to move to a higher level of maturity over time. Adaptations of the following diagram are used throughout this document to summarize maturity levels according to the themes and questions explored in each chapter:

The asset management framework can be likened to a continuum, whereby municipalities should aim to implement the components described in a subsequent maturity level. For example, municipalities that are not practicing asset management should strive to meet components at the basic level, and likewise, municipalities that currently meet the basic or intermediate levels should strive to advance their practices to meet the components of the next level. However, it should be noted that during this self-assessment process a municipality may decide to skip over maturity levels (i.e. move from basic to advanced, skipping intermediate). This is perfectly acceptable. Further, not every municipality will need to strive for the highest level of maturity in every area. For example, it may not make sense for a small municipality to meet certain advanced level components.

Readers can use the following descriptions of the maturity levels to guide their assessment throughout the various sections of this framework:

Municipalities that are not undertaking the components described in a particular section of this framework should focus on meeting the basic level requirements outlined in the maturity level diagram.

At the basic level of maturity, a municipality is undertaking the components of asset management shown in blue and will take steps to advance their asset management by implementing the components described under the intermediate level heading.

At the intermediate level of maturity, a municipality is currently meeting the requirements shown in yellow and to advance their asset management will take steps to implement the components described under the advanced level heading.

At the advanced level of maturity, a municipality is currently meeting the requirements shown in green.

These maturity framework visuals are found throughout this document. Preceding all maturity level diagrams is a self-assessment question for the reader to consider to help determine where their municipality best fits within the framework.

List of Acronyms and Abbreviations

AM Asset Management

ARL Annual Repayment Limit

BCI Bridge Condition Index

CCTV Closed-Circuit Television

CMMS Computerized Maintenance Management System

CoF Consequence of Failure

CPI Consumer Price Index

DCA Development Charges Act

FIR Financial Information Return

GIS Geographic Information System

IIMM International Infrastructure Management Manual

IJPA Infrastructure for Jobs and Prosperity Act

IT Information Technology

LMS Lifecycle Management Strategy

LOS Level(s) of Service

NRCPI Non-Residential Consumer Price Index

PoF Probability of Failure

PSAB Public Sector Accounting Board

RFP Request for Proposal

RRF Reserve/Reserve Fund

SAMP Strategic Asset Management Policy

SOLI State of Local Infrastructure

TCA Tangible Capital Asset

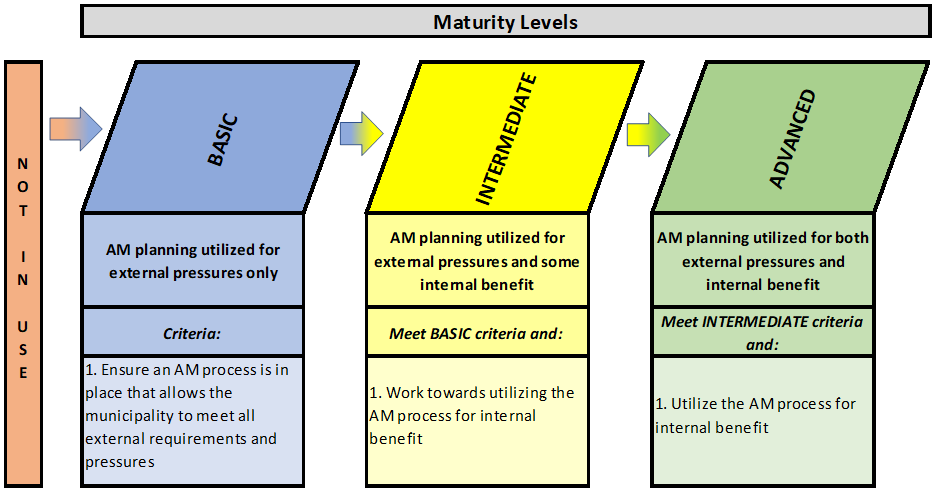

To what extent is the municipality utilizing the benefits of asset management planning within the organization?

Background

The importance of having an effective AM plan has been increasingly recognized internationally. This recognition was underscored by the 2014 release of the related International Standard ISO 55000, which “provides an overview of asset management, its principles and terminology, and the expected benefits from adopting asset management”.

Indeed, our communities, economies, and in many ways, our quality of life are all supported by various elements of infrastructure. It follows that governments have a great responsibility to properly manage their assets. This stewardship function falls heavily at the municipal level of government, where local citizens and taxpayers rely on the availability of critical services delivered by their municipality.

Consequently, municipalities need to be aware that there are many compelling reasons for engaging in a mature asset management process. These include the following internal benefits:

· Enhance financial performance;

· Assess and manage risk;

· Support sustainability of services:

· Meet service needs & promote customer satisfaction; and

· Support economic activity & promote satisfying lifestyle.

Levels of Maturity – Utilizing Benefits of Asset Management

To what extent is the municipality utilizing the benefits of asset management planning within the organization?

At the basic level of maturity, municipalities use asset management planning in response to external pressures, such as unexpected changes to service delivery, asset condition or risk; and/or financial conditions. Municipalities at the basic level need to ensure they have an asset management process in place that enables the ability and flexibility necessary to respond when external pressures demand it. However, at the basic level of maturity, these circumstances are often dealt with as part of the budget process at a high level.

At the intermediate level of maturity, asset management planning needs to be used to not only respond to external pressures, but also to derive some internal benefit. Municipalities are considered to be at the intermediate level of maturity if they recognize that asset management has integral connections to several other processes (e.g. budget, optimal maintenance schedules, planning, service delivery, etc.) and begin the process of integrating these processes.

At the advanced level of maturity, asset management is used for responding to external pressures and deriving internal benefits. Municipalities at this level should have identified all links between asset management and other processes, and should have integrated them to achieve internal efficiencies, track financial performance, focus on service delivery, and promote asset management sustainability.

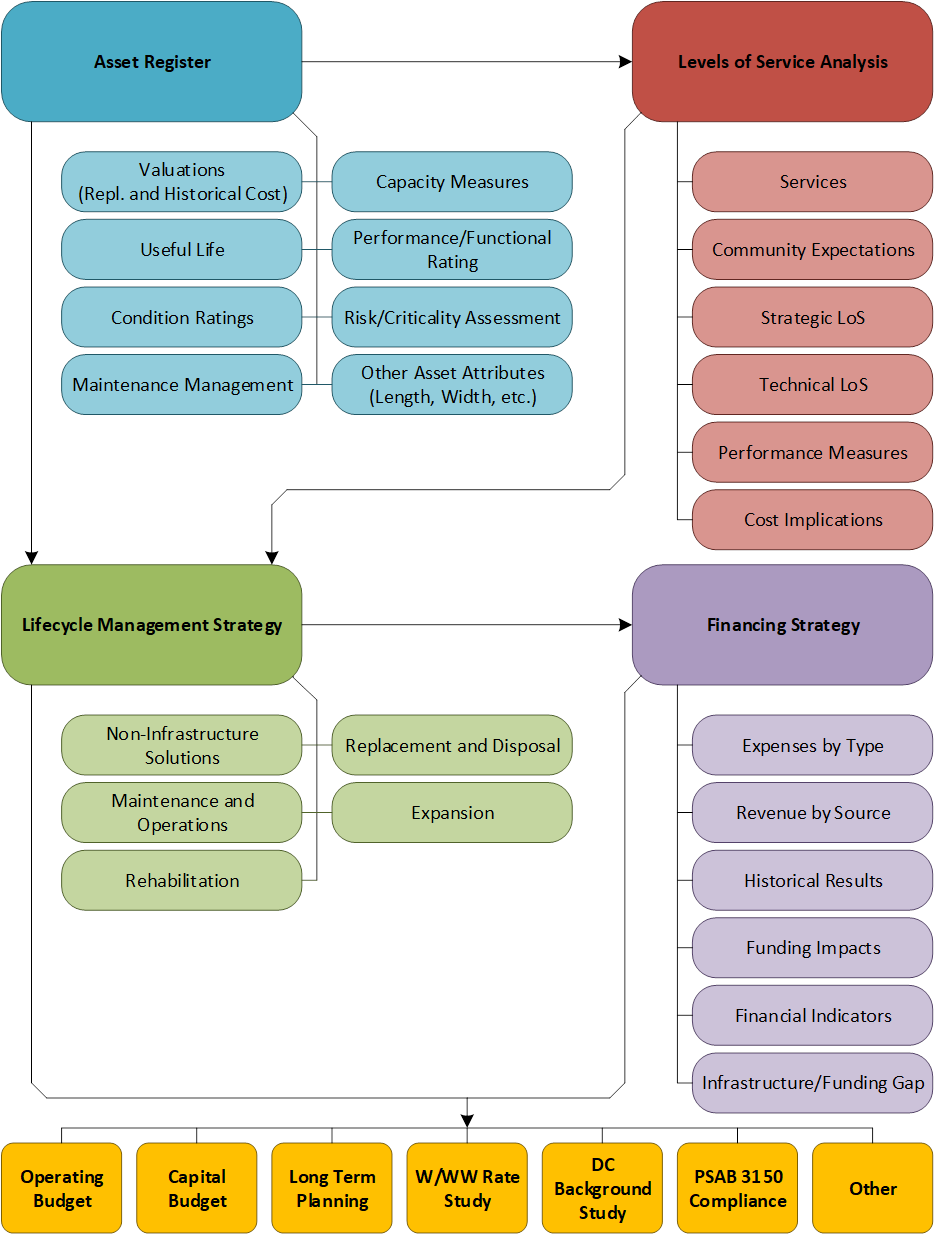

Asset Management Overview

There are a number of internal benefits to be gained by implementing asset management practices in addition to legislative and funding requirements. These potential benefits are discussed throughout this document. Figure 1-2 (below) highlights many of the elements of the asset management plan (discussed in detail in Chapters 3 through 6), how they interrelate, as well as other processes that could be integrated with asset management, such as:

· Operating Budget;

· Capital Budget;

· Long-term Capital Plans;

· User Fee Rate Studies (i.e. water, wastewater, stormwater);

· Development Charge Background Study; and

· PSAB 3150 Compliance Process.

Municipalities will begin to see added benefits as the processes above are integrated with their asset management planning processes.

As the relationship between a municipality’s AM process and the processes identified above is enhanced, the municipality will start seeing added internal benefits to the asset management process. A time will come when the internal benefits of AM planning will exceed the benefits from only responding to external pressures and requirements.

Keep in mind that a supporting comprehensive AM process ensures the development of a consistent and accurate AM plan. Figure 1-2 (below) shows the process and relationships among the component activities.

Figure 1‑2

Asset Management Process

To what extent is the municipality complying with asset management pressures/requirements in Ontario?

Background

The importance of implementing and maintaining a mature asset management process has been reinforced by the requirements of provincial legislation and federal/provincial grant application processes. Municipalities should be aware of these requirements to ensure they are in compliance with them.

Levels of Maturity – Complying with Asset Management Requirements

To what extent is the municipality complying with asset management pressures/requirements in Ontario?

At the basic level of maturity, municipalities engage in asset management activities to comply with the AM requirements under the Ontario Federal Gas Tax Agreement, ongoing provincial capital grant applications, and the Infrastructure for Jobs and Prosperity Act (IJPA) through O.Reg 588/17).

At the intermediate level of maturity, municipalities need to comply with the requirements outlined in the Federal Gas Tax Agreement for Ontario, the requirements for applying for provincial capital grants, and the requirements of the IJPA through O.Reg 588/17. In addition, the municipality should be actively progressing towards meeting other asset management requirements, such as the DCA requirements.

At the advanced level of maturity, the municipality should comply with the requirements outlined in the Federal Gas Tax Agreement for Ontario, the requirements for applying for provincial capital grants, the IJPA requirements through O.Reg 588/17, DCA requirements, as well as other applicable areas.

Asset Management Requirements

The following sections provide some detail on how asset management planning fits in with federal and provincial requirements:

Ontario: “Building Together”

In 2011, the Ontario government released “Building Together”, a long-term infrastructure plan which “sets out a strategic framework that will guide future investments in ways that support economic growth, are fiscally responsible, and respond to changing needs. A key element of this framework is ensuring good stewardship through proper asset management”. This document highlights the importance of addressing municipal infrastructure needs through a co-operative approach by all levels of government, and underpinned by AM strategy. In conjunction with this document, provincial capital grant opportunities have been made available where having an AM plan is a prerequisite before receiving funding.

As outlined in Ontario's Building Together: Guide for Municipal Asset Management Plans, the elements of a detailed asset management plan must include the following:

· Executive Summary:

o Typically, the final section to be prepared, and provides a succinct overview of the plan.

· Introduction:

o Explains how the goals of the municipality are dependent on infrastructure. This could include discussing how infrastructure assets support economic activity and improve quality of life. The municipality’s goals may already be set out in documents, including the strategic plan and/or the Official Plan, or may need to be developed in consultation with residents.

o Clarifies the relationship of the asset management plan to municipal planning and financial documents (e.g. how the plan impacts the budget, Official Plan and Infrastructure Master Plan).

o Describes to the public the purpose of the asset management plan (i.e. to set out how the municipality’s infrastructure will be managed to ensure that it is capable of providing the levels of service needed to support the municipality’s goals).

o States which infrastructure assets are included in the plan. Best practice is to develop a plan that covers all infrastructure assets for which the municipality is responsible. At a minimum, plans should cover roads, bridges, water and wastewater systems, and social housing.

o Identifies how many years the asset management plan covers and when it will be updated. At a minimum, plans must cover 10 years and be updated regularly. Best practice is for plans to cover the entire lifecycle of assets.

o Describes how the asset management plan was developed — who was involved, what resources were used, any limitations, etc.

o Identifies how the plan will be evaluated and improved through clearly defined actions. Best practice is for actions to be short-term (less than three years) and include a timetable for implementation.

· State of Local Infrastructure:

o See Chapter 3.

· Expected Levels of Service:

o See Chapter 4.

· Asset Management Strategy:

o See Chapter 5 – section renamed Lifecycle Management Strategy.

· Financing Strategy

o See Chapter 6.

Federal Gas Tax Agreement in Ontario

Asset management is included as part of the requirements to receive federal gas tax funding in Ontario. In the administrative agreement for the federal gas tax fund, asset management is defined as:

…a strategic document that states how a group of assets are to be managed over a period of time. The plan describes the characteristics and condition of infrastructure assets, the levels of service expected from them, planned actions to ensure the assets are providing the expected level of service, and financing strategies to implement the planned actions. The plan may use any appropriate format, as long as it includes the information and analysis required to be in a plan as described in Ontario's Building Together: Guide for Municipal Asset Management Plans.

Provisions of the federal gas tax administrative agreement related to asset management plans include:

· The costs to develop asset management plans are considered eligible expenditures for gas tax funding;

· In order to continue to be eligible for gas tax funding, municipalities must have developed an asset management plan by December 31, 2016; and

· Municipalities must provide a report to the Association of Municipalities of Ontario that an asset management plan is being used as a guide to infrastructure planning and investment decisions, including how federal gas tax funds are to be used.

Infrastructure for Jobs and Prosperity Act, 2015 (IJPA)

The Infrastructure for Jobs and Prosperity Act, 2015 (IJPA) was passed by the Province of Ontario June 4, 2015. As noted in section 1 of the IJPA, the Act has been enacted to “establish mechanisms to encourage principled, evidence-based and strategic long-term infrastructure planning that supports job creation and training opportunities, economic growth and protection of the environment, and incorporate design excellence into infrastructure planning”. The IJPA applies to the broader public sector of which municipalities as noted in subsection 6 (2)(a), are part. (Note: local boards are also included as noted in subsection 6 (2)(b), however for the discussion purposes within this chapter, only municipalities will be specifically referenced). For the purposes of the IJPA, the definition of municipalities is identified as being from the Municipal Act, 2001 in subsection 1 (1).

The IJPA outlines the need for an Infrastructure Asset Management Plan in subsection 6 (1):

Every broader public-sector entity prescribed for the purposes of this section shall prepare the infrastructure asset management plans that are required by the regulations and that satisfy the prescribed requirements.

Further, IJPA stipulates that the municipality shall provide the infrastructure AM plan to the province, as required by the Minister, and if required by regulations, shall also make the infrastructure AM plan available to the public.

The IJPA also presents a number of principles for municipalities to consider when making decisions related to infrastructure. Please refer to Chapter 2 for more details.

Requirements for the development of an asset management process are also outlined in a regulation of the IJPA (O.Reg 588/17):

1. A Strategic Asset Management Policy by July 1, 2019 (discussed in detail in Chapter 2);

2. Municipalities would be required to prepare an asset management plan in three phases:

a. Phase I would address core infrastructure assets (i.e. roads, bridges, culverts, wastewater, water, and stormwater) and would be required to be completed by July 1, 2021.

b. Phase II would expand on Phase I by including all infrastructure assets in the plan by July 1, 2023.

c. Phase III would require further details to be provided for all infrastructure assets by July 1, 2024.

3. Phase I (i.e. core infrastructure) and Phase II (i.e. all infrastructure) of the asset management implementation would include the following:

a. Current levels of service.

b. Current asset performance, using performance measures.

c. An asset inventory, including replacement cost, age, and condition.

d. Estimated lifecycle costs by asset category to maintain current levels of service for 10 years.

e. For municipalities with populations under 25,000: Assumptions regarding future changes in population or economic activity, and how they relate to estimated lifecycle costs to maintain current levels of service.

f. For municipalities with populations over 25,000: Population and employment forecasts (from Growth Plans, official plans, etc.), and the lifecycle costs required to maintain current levels of service in order to accommodate projected increases in demand caused by growth.

4. Phase III of the asset management implementation would include the following:

a. Proposed levels of service for the next 10 years, using provided metrics for core infrastructure and municipally created metrics for other infrastructure.

b. An explanation of why the proposed levels of service are appropriate, including risks, affordability and whether they are achievable.

c. The proposed performance of each category for each year over 10 years.

d. A lifecycle management strategy.

e. A financial strategy.

f. Document and address available funding as well as funding shortfalls.

g. For municipalities with populations under 25,000: A discussion of how assumptions regarding future changes in population and economic activity informed the preparation of the lifecycle management strategy and financial strategy.

h. Municipalities with populations over 25,000: Estimated lifecycle costs to achieve proposed levels of service in order to accommodate projected increases in demand caused by population and employment growth, the funding projected to be available (by source)as a result of increased population and economic activity, and an overview of risks associated.

i. An explanation of any other key assumptions.

5. Updates, approvals and public availability:

a. Review and update the asset management plan at least every 5 years.

b. The asset management plan (or update) must be endorsed by the executive lead of the municipality, and approved by Council resolution.

c. Municipalities would be required to provide Council with an annual update on asset management planning progress, by July 1st of each year.

d. Municipalities would be required to post their strategic asset management policy and asset management plan on the municipality’s website, if one exists, and make copies of these documents available to the public, if requested.

Please note that the specific requirements of the regulation are discussed in the introduction/overview sections of each chapter throughout this framework document.

Development Charges Act (DCA)

The recent changes to the DCA in December 2016 (new clause 10(2) (c.2)) requires that a Development Charge Background Study must include an asset management plan related to new infrastructure.

Subsection 10 (3) of the DCA provides:

(3) The asset management plan shall,

(a) deal with all assets whose capital costs are proposed to be funded under the development charge by-law;

(b) demonstrate that all the assets mentioned in clause (a) are financially sustainable over their full lifecycle;

(c) contain any other information that is prescribed; and

(d) be prepared in the prescribed manner.

There are no prescribed requirements at this time for all services, except transit. Therefore, the municipality defines the approach to include within the background study.

For transit, the amended regulations provide for a prescriptive evaluation. In regard to the DCA requirements for asset management for the Transit Service, Ontario Regulation 82/98 (as amended) provides the following:

8(3) If a council of a municipality proposes to impose a development charge in respect of transit services, the asset management plan referred to in subsection 10 (2) (c.2) of the Act shall include the following in respect of those services:

1. A section that sets out the state of local infrastructure and that sets out,

i. the types of assets and their quantity or extent,

ii. the financial accounting valuation and replacement cost valuation for all assets,

iii. the asset age distribution and asset age as a proportion of expected useful life for all assets, and

iv. the asset condition based on standard engineering practices for all assets.

2. A section that sets out the proposed level of service and that,

i. defines the proposed level of service through timeframes and performance measures,

ii. discusses any external trends or issues that may affect the proposed level of service or the municipality’s ability to meet it, and

iii. shows current performance relative to the targets set out.

3. An asset management strategy that,

i. sets out planned actions that will enable the assets to provide the proposed level of service in a sustainable way, while managing risk, at the lowest life cycle cost,

ii. is based on an assessment of potential options to achieve the proposed level of service, which assessment compares,

A. life cycle costs,

B. all other relevant direct and indirect costs and benefits, and

C. the risks associated with the potential options,

iii. contains a summary of, in relation to achieving the proposed level of service,

A. non-infrastructure solutions,

B. maintenance activities,

C. renewal and rehabilitation activities,

D. replacement activities,

E. disposal activities, and

F. expansion activities,

iv. discusses the procurement measures that are intended to achieve the proposed level of service, and

v. includes an overview of the risks associated with the strategy and any actions that will be taken in response to those risks.

4. A financial strategy that,

i. shows the yearly expenditure forecasts that are proposed to achieve the proposed level of service, categorized by,

A. non-infrastructure solutions,

B. maintenance activities,

C. renewal and rehabilitation activities,

D. replacement activities,

E. disposal activities, and

F. expansion activities,

ii. provides actual expenditures in respect of the categories set out in sub-subparagraphs i A to F from the previous two years, if available, for comparison purposes,

iii. gives a breakdown of yearly revenues by source,

iv. discusses key assumptions and alternative scenarios where appropriate, and

v. identifies any funding shortfall relative to financial requirements that cannot be eliminated by revising service levels, asset management or financing strategies, and discusses the impact of the shortfall and how the impact will be managed.

Government of Canada, Infrastructure Canada, 2014, Administrative Agreement on the Federal Gas Tax Fund (Canada‑Ontario‑The Association of Municipalities of Ontario‑The City of Toronto), http://www.infrastructure.gc.ca/prog/agreements-ententes/gtf-fte/2014-on-eng.html

International Organization for Standardization (ISO), 2014, ISO 55000:2014, Asset management – Overview, principles and terminology, http://www.iso.org/iso/catalogue_detail?csnumber=55088

Province of Ontario, 1996, Development Charges Act, https://www.ontario.ca/laws/statute/97d27

Province of Ontario, Ministry of Infrastructure, https://www.ontario.ca/page/ministry-infrastructure

Province of Ontario, Ministry of Infrastructure, 2012, Building Together: Guide for Municipal Asset Management Plans, https://www.ontario.ca/page/building-together-guide-municipal-asset-management-plans