Final – May 15 2018

7 Asset Management Integration

7.3 Capital Budget Integration

7.4 Operating Budget Integration

7.5 Strategic Plan Integration

Final – May 15 2018

7 Asset Management Integration

7.3 Capital Budget Integration

7.4 Operating Budget Integration

7.5 Strategic Plan Integration

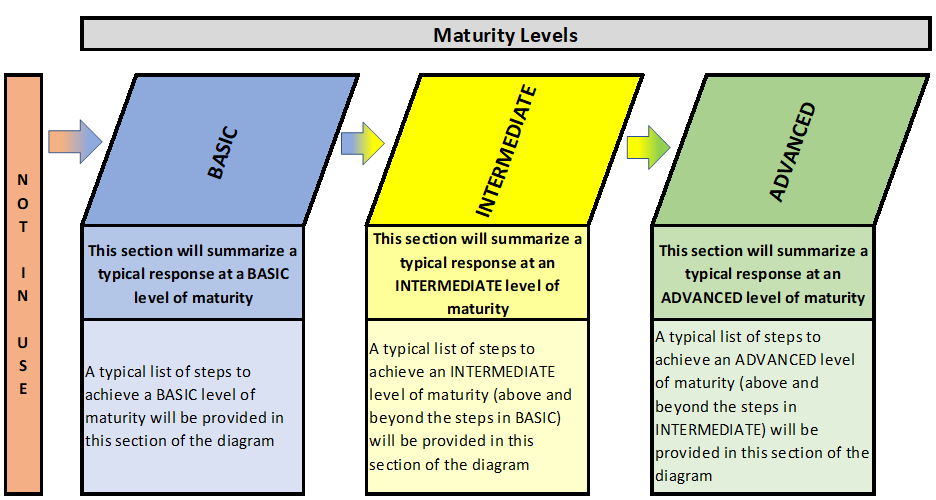

This framework is intended for municipalities of all sizes and maturity levels. The use of the maturity diagrams within this framework can help municipalities identify their current levels of maturity for each AM area. In addition, the diagrams provide possible approaches for municipalities to undertake to move to a higher level of maturity over time. Adaptations of the following diagram are used throughout this document to summarize maturity levels according to the themes and questions explored in each chapter:

This document is intended to help municipalities make progress on their asset management planning. By enhancing the readers’ understanding of asset management maturity, they can more accurately determine their current, and work toward achieving the desired or appropriate, level of maturity for their municipality.

The asset management framework can be likened to a continuum, whereby municipalities should aim to implement the components described in a subsequent maturity level. For example, municipalities that are not practicing asset management should strive to meet components at the basic level, and likewise, municipalities that currently meet the basic or intermediate levels should strive to advance their practices to meet the components of the next level. However, it should be noted that during this self-assessment process a municipality may decide to skip over maturity levels (i.e. move from basic to advanced, skipping intermediate). This is perfectly acceptable. Further, not every municipality will need to strive for the highest level of maturity in every area. For example, it may not make sense for a small municipality to meet certain advanced level components.

Readers can use the following descriptions of the maturity levels to guide their assessment throughout the various sections of this framework:

Municipalities that are not undertaking the components described in a particular section of this framework should focus on meeting the basic level requirements outlined in the maturity level diagram.

At the basic level of maturity, a municipality is undertaking the components of asset management shown in blue and will take steps to advance their asset management by implementing the components described under the intermediate level heading.

At the intermediate level of maturity, a municipality is currently meeting the requirements shown in yellow and to advance their asset management will take steps to implement the components described under the advanced level heading.

At the advanced level of maturity, a municipality is currently meeting the requirements shown in green.

These maturity framework visuals are found throughout this document. Preceding all maturity level diagrams is a self-assessment question for the reader to consider to help determine where their municipality best fits within the framework.

Asset management should not be conducted as a stand-alone process. The elements of asset management, including identifying capital and operating budget requirements, financing options, delivery of services, risk assessment, and stewardship of assets impact other key processes across a municipality, and in some cases, are indelibly linked. As a municipality pursues its strategic goals, the integration of asset management with other processes helps facilitate a co-ordinated and consistent approach to meeting these goals.

From an operational perspective, integrating systems with common data can provide an opportunity for identifying efficiencies that may otherwise be missed. For example, by integrating related systems, data may only need to be recorded and updated once for various uses. This may reduce the staff effort needed to perform related data management duties. Further, having a more integrated set of systems reduces the chance for inconsistencies and errors between systems. In addition, integrated systems may facilitate more timeliness and help to ensure consistency of outputs when reporting is required from these systems.

When considering integration, it is important to keep in mind that this could entail a two-way interaction between asset management and other related processes. The impacts of changes to any one process should automatically trigger consideration of making corresponding adjustments to related policies and/or procedures. This chapter discusses the importance of integrating asset management planning with:

· Capital budget;

· Operating budget;

· Strategic plan; and

· Other policies and processes.

Infrastructure for Jobs and Prosperity (IJPA) Act and O. Reg 588/17 Requirements

O.Reg 588/17 outlines the following requirements with respect to AM Integration:

A Strategic Asset Management Policy (SAMP) must be developed and adopted by July 1, 2019 and reviewed and updated at least every 5 years. The SAMP should outline a number of potential areas of integration, including the requirement to/ for:

1. Identify which municipal goals, plans or policies the AM plan would support (e.g. official plan, strategic plan, master plans, etc.);

2. A process for how the AM plan is to be considered in the annual budget and any applicable long-term financial plans;

3. The principles to guide AM planning in the municipality, including principles identified in section 3 of the IJPA;

4. A process to ensure alignment of AM planning with water and wastewater financial plans, including any financial plans prepared under the Safe Drinking Water Act, 2002.

5. A process to ensure alignment of AM planning with Ontario’s land-use planning framework, including any relevant policy statements issued under section 3(1) of the Planning Act; Provincial plans as defined in the Planning Act; and, municipal official plans;

6. A discussion of capitalization thresholds used to determine which assets should be included in the AM plan and how the thresholds compare to the municipality’s Tangible Capital Asset policy;

7. A commitment to coordinate planning between interrelated infrastructure assets with separate ownership structures by pursuing collaborative opportunities with upper-tier municipalities, neighbouring municipalities, and jointly-owned municipal bodies.

Every municipality shall prepare an asset management plan in respect of its core municipal infrastructure assets, as defined in the Regulation, by July 1, 2021, and in respect of all of its other municipal infrastructure assets by July 1, 2023.

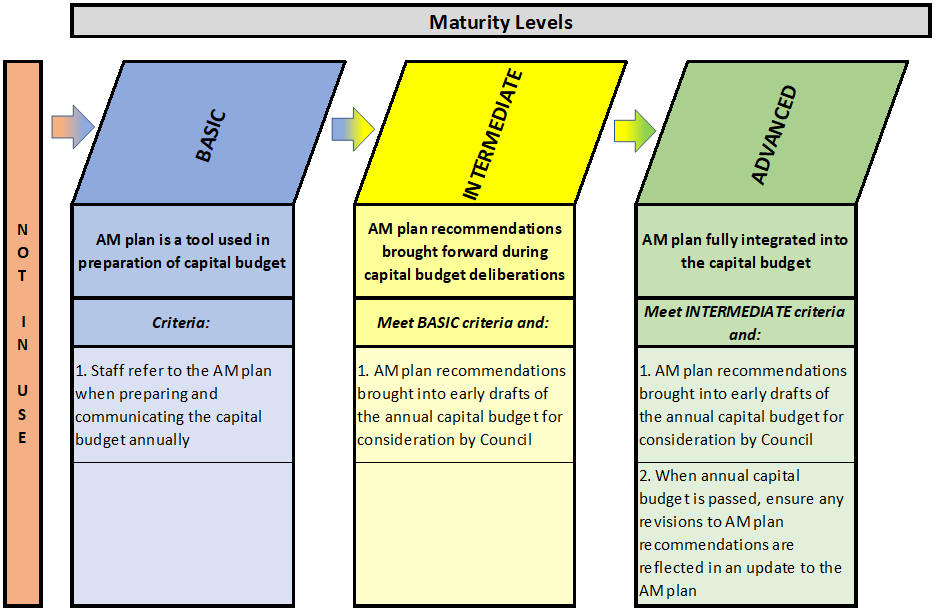

To what extent is the asset management plan integrated into the capital budget?

Background

The asset management plan forms the foundation for prioritizing long-term capital project requirements. Capital priorities and spending can be forecasted through the preparation of lifecycle management strategies, taking factors such as risk, condition, and service levels into account. This mirrors many of the decisions made when preparing a capital budget and long-term forecast each year as part of the budget process.

Levels of Maturity

To what extent is the asset management plan integrated into the capital budget?

At the basic level of maturity, the asset management plan is used as a source of information in preparing the capital budget. Typically, staff refer to relevant elements of the asset management plan as they prepare and communicate details related to the capital budget. However, at the basic level of maturity, as the capital budget progresses through the deliberation process, the connection to the asset management plan may be lost.

At the intermediate level of maturity, asset management recommendations are brought forward during the early drafts of the annual capital budget deliberations with Council. This provides the opportunity to link the benefits gained from proper asset management into the capital budget process, and the opportunity to assess the related impacts on each at the Council level. At the intermediate level of maturity, as the capital budget process progresses its connection and relationship to the asset management plan may still be broken.

At the advanced level of maturity, the asset management plan is fully integrated into the annual capital budget. Asset management recommendations are brought forward during the early drafts of the annual capital budget deliberations with Council. This provides the opportunity to link the benefits gained from proper asset management into the capital budget process, and the opportunity to assess the related impacts on each at the Council level. When the annual capital budget is passed, any impacts to the asset management plan recommendations should be identified and included in an update to the asset management plan.

Asset Management and the Capital Budget

The capital budget preparation process mirrors the processes required to prepare an asset management plan. In a way, they can be treated as one and the same process, in that:

• Capital assets are analyzed to identify priorities;

• Service levels to be provided to the community are identified; and

• A recommended approach to financing capital priorities is determined.

The combination of the state of local infrastructure, levels of service analysis, lifecycle management strategies, and financing strategies outlined in the asset management plan form a logical foundation upon which the capital budget (and long-term capital forecast) can be prepared.

As municipalities deliberate on the capital budget, it is common for capital priorities to change or for financing alternatives to be amended based on ongoing communication and interaction with Council. This can occur for many reasons such as new financial constraints, changing direction from Council, legislative changes, levels of service amendments. Depending on the municipality’s level of integration, updates to both the capital budget and AM plan may be required to keep them aligned when the capital budget is passed. Keeping these processes aligned allows staff to coordinate the impact of Council decisions on the capital budget over a long-term time horizon from an asset condition/risk, service level, and available financing perspective, all within the AM plan.

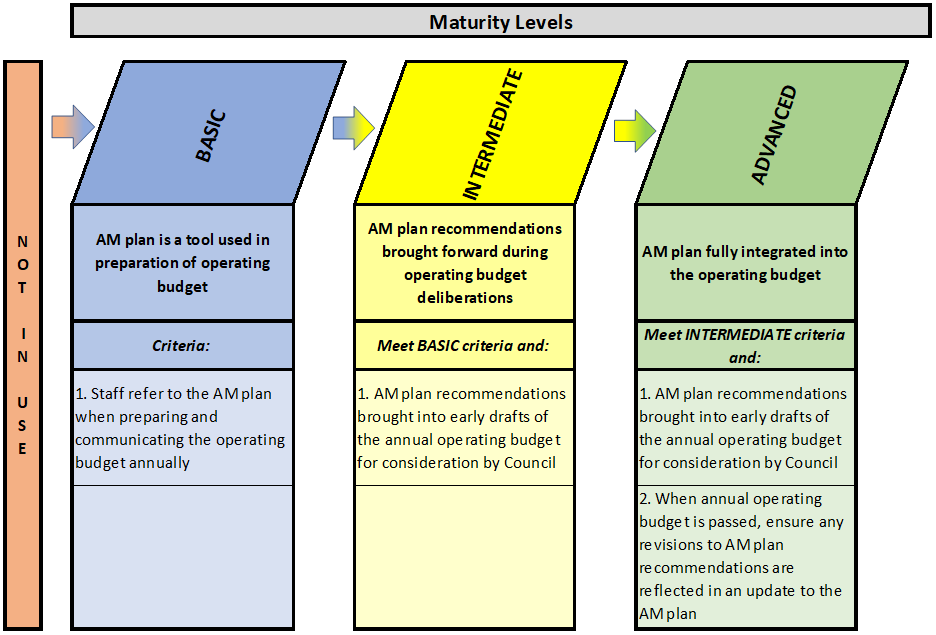

To what extent is the asset management plan integrated into the operating budget?

Background

Asset management plans provide key inputs into the operating budget. This is due to the fact that lifecycle management strategy outlines non-infrastructure solutions, asset maintenance needs, and other operational costs, which provides a more exact level of operating expenditure requirement than simply basing maintenance budgets on previous year plus an inflationary increase.

Levels of Maturity

To what extent is the asset management plan integrated into the operating budget?

At the basic level of maturity, the asset management plan is used as a source of information in the preparation of the operating budget. Typically, staff refer to relevant elements of the asset management plan as they prepare and communicate details related to the operating budget. However, at the basic level of maturity, the connection to the asset management plan may be lost as the operating budget progresses through the deliberation process.

At the intermediate level of maturity, asset management recommendations are brought forward during the early drafts of the annual operating budget deliberations with Council. This provides the opportunity to link the benefits gained from proper asset management into the operating budget process, and the opportunity to assess the related impacts on each at the Council level. At the intermediate level of maturity, as the operating budget process progresses its connection and relationship to the asset management plan may be broken.

At the advanced level of maturity, the asset management plan is fully integrated into the annual operating budget. Asset management recommendations are brought forward during the early drafts of the annual operating budget deliberations with Council. This provides the opportunity to link the benefits gained from proper asset management into the operating budget process, and the opportunity to assess the related impacts on each at the Council level. When the annual operating budget is passed, any impacts to the asset management plan recommendations are identified and reflected in an update to the asset management plan.

Asset Management and the Operating Budget

Operating impacts identified though the asset management process include:

· Non-infrastructure solutions;

· Asset maintenance and operating needs; and

· Financing strategy related implications.

Non-infrastructure solutions that are considered part of the lifecycle management strategy will generally have operating-related financial impacts, while affecting capital related decisions, such as useful life and lifecycle costing. Non-infrastructure solutions may include additional costs (e.g. study costs), or cost savings (e.g. fewer inspections of low risk assets). In either circumstance, these impacts should be reflected in the lifecycle management strategy of the AM plan and will have implications on future operating budgets. Non-infrastructure solutions are discussed in more detail within Chapter 5.

Similar to non-infrastructure solutions, asset maintenance and operating-related needs have financial impacts on the operating budget. These impacts may be in the form of costs (e.g. road crack sealing program) or savings (e.g. hydro impacts from LED streetlight program). Whether costs or savings, the impacts are reflected in the lifecycle management strategy and have implications on future operating budgets.

A funding analysis is useful to undertake as part of the financing strategy of the AM plan and as part of the operating budget (i.e. analyses of taxation, user fees, other revenue, debt, and reserves/reserve funds). Both processes can have very similar funding strategies. However, Council may ultimately pass an operating budget that could look quite different from the AM plan estimates. Some areas of impact include:

· Taxation levy and user fee amounts: The operating budget will determine the actual taxation levy or user fee rates (e.g. water and wastewater, recreation facilities, etc.) for the year which might differ from estimates within the AM plan.

· New debt: The anticipated issuance of debt to fund budgeted capital projects will create future principal and interest costs to be included in current and future budgets. These financial impacts may not have been anticipated in the preparation of the AM plan, or proposed debt within the AM plan may not be approved within the budget process.

· Reserve/reserve funds: The reserve/reserve fund strategies will also impact on the operating budget, as the funding of the capital reserve funds from the operating budget will need to be incorporated. These strategies may differ between what has been originally projected in the AM plan and what is ultimately approved to be included in the operating budget.

· Other revenues: Grants or other irregularly available revenues may become known during the budget process that may not be reflected in the AM plan, or vice versa.

As municipalities deliberate on the operating budget, it is common for operating priorities to change, variables (such as inflation) to be amended, or financing alternatives to be edited. These changes can occur for many reasons such as new financial constraints, changing direction from Council, legislative changes, or levels of service amendments. It is important to revise the asset management plan accordingly to ensure consistency between the asset management plan and final operating budget passed by Council.

Timing and sequence determines whether or not the AM plan or budget is most accurate (i.e. which one was created last, based on most recent data, assumptions and variables?). Full integration of the operating budget with the AM plan ensures both use consistent and accurate results. Therefore, it is recommended that as one is updated, the other is also.

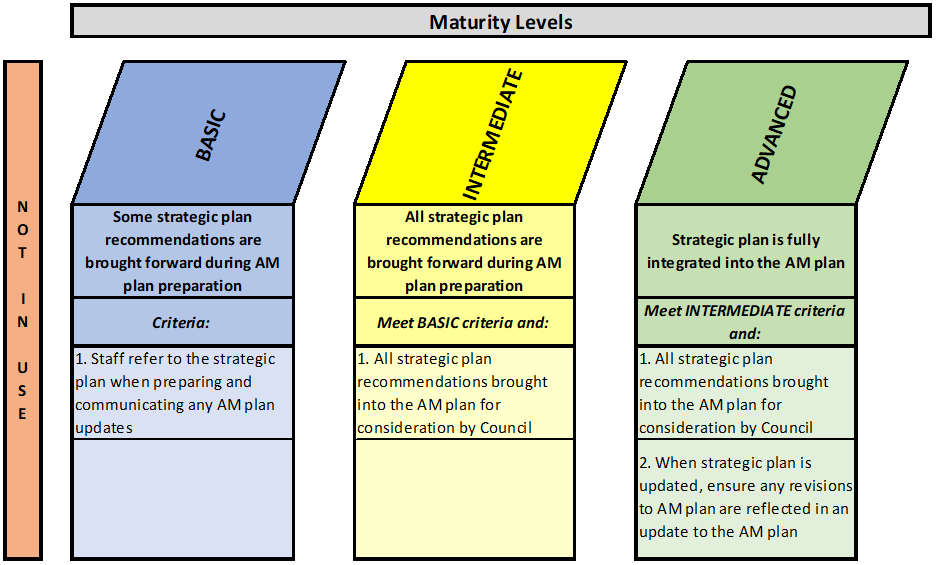

To what extent is the asset management plan integrated with the municipality's strategic plan?

Background

A strategic planning process can help a municipality establish an overall corporate vision, mission, and goal. It is a critical process that examines where a municipality is now, where it wants to go, and how it should get there. It will help the municipality identify action priorities that are consistent with the established corporate goals. A strategic plan is a “living document” that is regularly updated (usually every 5 years). AM-related missions and goals can become a component of the overall corporate strategic plan. Moreover, the decisions made within the strategic planning process can provide valuable input into the AM planning process.

Levels of Maturity

To what extent is the asset management plan integrated with the municipality's strategic plan?

At the basic level of maturity, some strategic plan recommendations are brought forward during the preparation of the asset management plan. Typically, staff refer to relevant elements of the strategic plan as they prepare or update the asset management planning process. However, there may be some gaps or inconsistencies between the strategic plan and the asset management planning process. At this level, asset management is likely not a key component to the strategic plan.

At the intermediate level of maturity, all strategic plan recommendations are brought forward during the preparation of the asset management plan. Staff should be aware of all interrelated strategic plan recommendations and should strive to maintain consistency between the objectives of the strategic plan and the asset management planning process, where applicable. This should allow Council to consider the asset management plan since they will know that it conforms to provisions of the strategic plan.

At the advanced level of maturity, all strategic plan recommendations are brought forward during the preparation of the asset management plan. Staff are aware of all interrelated strategic plan recommendations and strive to maintain consistency between the objectives of the strategic plan and the asset management plan. This should allow Council to consider the asset management plan since they will know that it conforms to provisions of the strategic plan. In addition, when there are updates to the strategic plan, possible updates to related provisions in the asset management planning process should be considered.

Asset Management and Strategic Planning

The overall corporate vision, mission, and goals of the municipality should be considered when updating or creating an asset management plan. Typically this information is recorded in a municipality’s strategic plan. Like the strategic plan, the asset management planning process has a long-term view. To meet strategic planning goals, all necessary infrastructure must be in place to successfully provide necessary service levels. Thus, there must be a connection between the two processes. Such connection can happen by updating related provisions of the asset management plan any time the strategic plan is modified. Doing so will maintain consistency between the plans. This can be done by aligning the timing of a new strategic plan with a corresponding planned update to a municipality’s AM plan. It should be noted, however, that aligning the timing does not necessarily mean undertaking both at the same time as this could be difficult to do. Alignment in this context refers to the need to recognize the latest updates of the other document, whenever these take place.

The levels of service analysis is a key component to asset management (see Chapter 4). Initial sections of Chapter 4 discuss the identification of municipal services and the process of determining community expectations on those services. This process, while directly related to asset management, can also form future updates to the strategic plan. If the ultimate objective of a municipality is to provide services to the community, overall levels of service and changes to levels of service should be reflected in the strategic plan. Conversely, to initiate the process in Chapter 4 (of establishing a levels-of-service analysis), future anticipated strategic plan updates could form the foundation of this analysis. This methodology can produce the additional benefit of ensuring that the levels of service expectations would have been discussed and approved by Council before making its way into the AM planning process. Consequently, the levels of service analysis would then be consistent with Council’s vision for the municipality.

A second aspect to the strategic planning process is the possibility to link the strategic plan to departmental goals and objectives and then link individual staff goals and objectives to these departmental goals and objectives. With this philosophy, municipal staff work towards departmental goals, which in turn assists departments in working towards corporate goals, which in turn are in line with the overall organizational mission and vision within the strategic plan. This extended process could also be used to enhance the levels of service analysis within AM planning, as discussed in Chapter 4. What the various departments and staff members do on a day-to-day basis to meet respective departmental goals and objectives could inform the technical levels of service analysis, which demonstrates what the municipality will do to move towards expected levels of service.

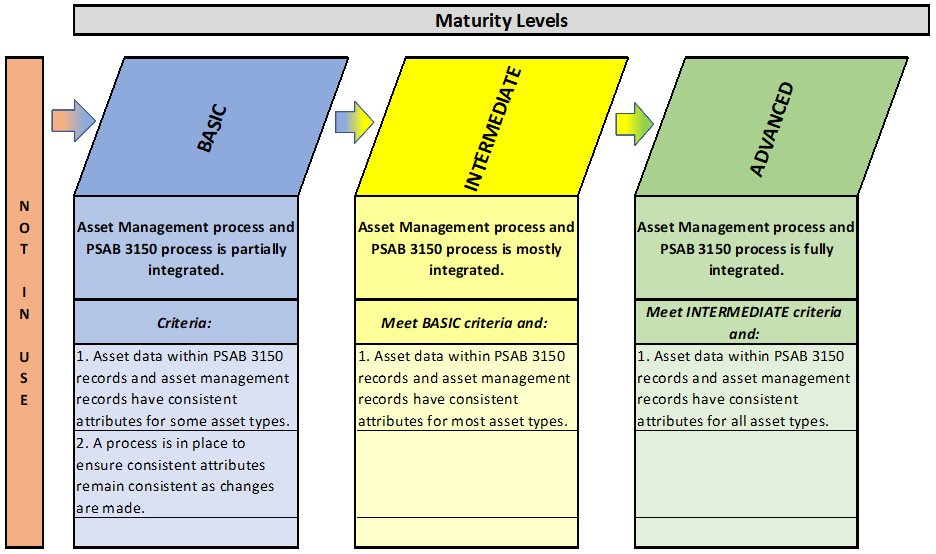

To what extent is the asset management plan integrated with PSAB 3150 asset data?

Background

Both the PSAB 3150 requirements and the asset management requirements are based on a list of assets with key attributes and asset costing. However, the approaches of attribute identifying and costing differ in each requirement. Both require the ability to keep the asset listing up-to-date and accurate, so that resulting calculations are accurate. Municipalities must determine if there is enough commonality among the PSAB 3150 process and AM process to justify integration.

Levels of Maturity

To what extent is the asset management plan integrated with PSAB 3150 asset data?

At the basic level of maturity, the asset management process is partially integrated with PSAB 3150. Asset attributes are consistent for some asset types, and a process exists to ensure consistency as change occurs.

At the intermediate level of maturity, the asset management process is mostly integrated with PSAB 3150. Asset attributes are consistent for most asset types, and a process exists to ensure attribute consistency as changes are made.

At the advanced level of maturity, the asset management process is fully integrated with PSAB 3150. Asset attributes are consistent for all asset types.

Asset Management and PSAB 3150

Integrating the asset management and PSAB processes enables a municipality to use asset attributes that are consistent between processes to perform calculations and meet legislative requirements. While the calculations (i.e. lifecycle costing versus amortization) and the costing (replacement cost versus historical cost) are quite different, information such as asset additions, disposals, asset impairments, length, width, and material type can be useful in both cases. Rather than having this data updated and maintained twice each time an asset changes, integration allows the ability to only update and maintain this data once.

Some areas to consider when determining whether to integrate asset management and PSAB 3150 data:

· The level of effort to establish the integration. Some municipalities have determined that the most efficient approach to this integration is to use a municipality’s asset management data to “restate” PSAB 3150 asset data. This involves recalculating historical cost, accumulated amortization, net book value, etc. based on asset management data. External auditors should be consulted during this exercise.

· The amount of savings (time and resources) from having the integration in place. If a municipality has under a dozen capital transactions a year, the amount of time it takes to establish the integration may greatly exceed the annual savings with respect to time and resources.

· Establishing a common asset identifier (see Chapter 3).

· What will the relationship be between asset processes? Will the asset data reside in one consolidated register, or will the data reside in multiple registers that “speak to each other”?

· Determine if any asset management tools may make this process more efficient (see Chapter 9).

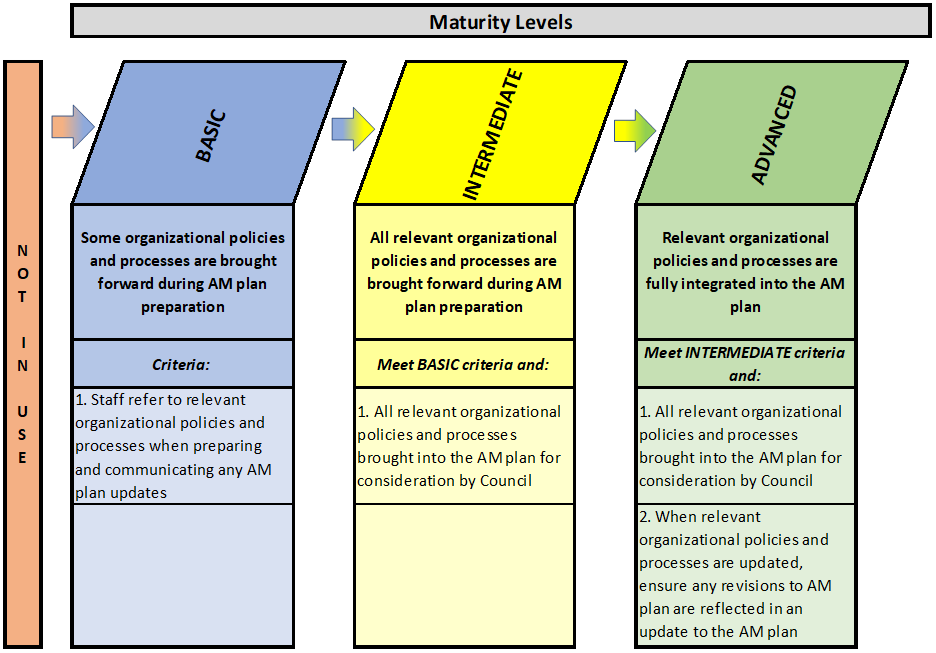

To what extent is the asset management plan integrated with other policies/processes?

Background

A municipality ability to meet its goals and service levels largely depends on whether it has sufficient infrastructure/assets with appropriate conditions, functionalities and capacities, and whether it can mitigate risk. This infers that many policies and processes, from all aspects of the municipality, will have a connection to elements of the asset management planning process. The more asset management is integrated into the fabric of municipal operations, the more efficient and effective these policies and processes become.

Levels of Maturity

To what extent is the asset management plan integrated with other policies/processes?

At the basic level of maturity, some organizational policies and processes are brought forward into the asset management planning process. Typically, staff refer to relevant organizational policies and processes as they prepare or update the asset management plan. However, staff may not be in a position to be aware of all potentially interrelated policies and processes, and thus some inconsistencies may occur between objectives of these policies and processes and the asset management planning process.

At the intermediate level of maturity, all organizational policies and processes are brought forward within the asset management planning process. Staff are aware of all interrelated policies and processes and strive to maintain consistency between the objectives of these policies and processes and the asset management planning process. This allows Council to consider the asset management plan, since they will know that it conforms to provisions of other policy directions.

At the advanced level of maturity, all organizational policies and processes are brought forward during the asset management planning process. Staff are aware of all interrelated policies and processes and strive to maintain consistency between the objectives of these policies and processes and the asset management plan. This allows Council to consider the asset management plan, since they will know that it conforms to provisions of other policy directions. In addition, when there are updates to other policies and processes, consideration can be given to making corresponding updates to related provisions in the asset management planning process. In essence, full integration of policies and plans across the municipality is the goal.

Asset Management and Other Municipal Processes

The following list provides examples of municipal processes, policies or strategies that have some connection to the AM process:

· Official Plan (and Secondary Plans);

· Purchasing (Procurement) Policy;

· Service Standards Policy;

· Master Plans (Transportation, Fire, Parks, Recreation, etc.);

· Fees & Charges Bylaws/Studies;

· Growth/Servicing Plans;

· Financial Policies/Strategies:

o Use of reserves/reserve funds;

o Use of debt;

o Use of Gas Tax funds;

o Grant application policy;

o Overall budget funding (or Council direction) policies.

These processes, if used and integrated into the asset management planning process, ensure not only increased accuracy of future asset management plans, but they also provide Council with the comfort that all municipal policies they have approved were followed in the development of the AM plan.